5 Components of Financial Literacy Critical to Future Success

Table of Contents

Why is Financial Literacy Important to your success?

Financial literacy is important to your success by empowering you to avoid financial mistakes, prepare for emergencies, and achieve your financial goals. Furthermore, financial literacy enables individuals to understand essential financial skills and concepts, reducing fraud risk and supporting life goals like education, retirement, debt management, and operating personal businesses.

In addition, this financial knowledge not only simplifies financial management but also reduces stress levels. Hence, financial literacy can enhance overall well-being, boost confidence in one’s ability to make sound financial decisions, and enable them to pursue financial goals which align with their vision for a happy life.

However, lack of financial literacy will often lead to overspending, debt accumulation, poor credit, bankruptcy (a costly and time-consuming legal process for those unable to pay debts, which can significantly damage a person’s credit score for years to come), and housing foreclosure, posing significant risks to one’s financial stability.

Understanding Financial Literacy

Financial literacy encompasses various skills including investments, savings, various types of debt, credit scores, budgeting strategies, and other associated financial concepts. Additionally, it also supports creating financial plans, holding oneself accountable, and approaching major life choices with confidence.

Investments

Investing is the first component of financial literacy and involves purchasing assets which increase in value over time, providing returns in the form of income payments (such as dividends) or capital gains. It can also involve spending time or money to improve one’s own life or others’ lives, particularly in the realm of finance, where it involves the purchase of securities, real estate, and other valuable items. Experts recommend investing 10% to 15% of your income.

IRA and Roth IRA Investment Accounts

A Traditional IRA allows individuals to direct pre-tax income towards tax-deferred investments, with no capital gains or dividend income taxes assessed until the beneficiary withdraws.

A Roth IRA is a tax-free retirement account that allows individuals aged 59½ or older to withdraw their money at any time, provided they have owned the account for 5 years.

Ownership Investments

Ownership investments involve owning assets expected to grow in value. These include stocks, real estate, precious metals, collectables, and businesses. Stocks give investors a stake in a company’s profits and gains. Real estate can be rented or sold for higher net profits. Precious metals, art, collectables, etc. are considered ownership investments if sold for profit.

Lending Investments

Lending investments involve lending money to another entity with the expectation of repayment. The lender charges interest on the loan, generating a profit once the loan is repaid. This type of investment is often low risk and offers low rewards.

Examples include bonds, certificates of deposit, and Treasury Inflation-Protected Securities (TIPS). Bonds allow corporations or governments to use their money with the expectation of profit after a set period with a fixed interest rate. Certificates of deposit lock investors’ money in a savings account for a set period with a higher interest rate. TIPS are bonds provided by the U.S. Treasury to protect investors against inflation, ensuring they receive their principal and interest back when their investment matures over time.

Pooled Investments

Pooled investment, such as mutual funds, pension funds, private funds, unit investment trusts (UITs), and hedge funds, allow multiple investors to gain advantages they wouldn’t have as individual investors.

A fund manager chooses the type of stocks, bonds, and other assets for the client’s portfolio, while charging a fee. Pension plans are retirement accounts established by employers, while private funds are composed of hedge funds and private equity funds. Unit investment trusts provide a fixed portfolio with a specified period of investment, sold as redeemable units. Hedge funds group client money to make risky investments using long and short strategies along with leverage to achieve higher returns.

Savings

Savings is the second component of financial literacy and involves spending less than you earn and setting aside the difference into high-yield savings accounts for stability and achieving short-term goals. Establishing an emergency savings fund with a goal of accumulating three to six months’ worth of expenses can provide peace of mind while navigating unexpected expenses without taking on debt. The Federal Reserve reports that 54% of individuals have three months’ worth of emergency reserves.

Traditional Savings Accounts

Traditional savings accounts are the most common type of savings account, with insured savings up to $250,000 per depositor if the bank is a member of the Federal Deposit Insurance Corp (FDIC) or the National Credit Union Administration (NCUA). These accounts provide easy access to cash and usually allow up to six withdrawals per statement cycle.

Interest rates on basic savings accounts are generally low compared to other savings products. Many of the highest-yielding savings account rates are found at online banks. It is essential to shop around to find the best account for you.

Online Savings Accounts

Online banks offer a convenient way to manage your money from anywhere, with the added benefit of being safe at federally-insured banks and credit unions. As long as you follow the FDIC or NCUA guidelines, online savings accounts tend to offer higher yields than those at physical branches. However, withdrawals are typically limited to six per statement cycle, so it’s essential to understand the terms of your account to avoid penalties. Online savings accounts are a convenient option for those comfortable with digital banking.

High-yield Savings Accounts

High-yield savings accounts offer higher interest rates, allowing faster savings growth without compromising safety and liquidity. However, some banks may limit withdrawals or electronic transfers per statement cycle. At a member-FDIC bank, your money remains safe even if the bank fails, as long as you adhere to FDIC limits and guidelines.

Student Savings Accounts

Student savings accounts offer simplified banking for young people with modest financial means, with no minimum opening deposits or monthly service fees. However, these accounts are less common than student checking accounts.

Certificate of Deposit (CD) Accounts

A certificate of deposit (CD) is a type of savings account offering higher yields compared to traditional accounts due to the agreement to keep money locked up for a specific term, typically three months to five years or longer. As a result, CDs have reduced liquidity, meaning funds cannot be withdrawn without penalty. Longer terms, like five-year CDs, may offer higher yields but would require the money to be untouched for five years. FDIC-insured CDs are safe, but early withdrawal penalties may apply. CDs are suitable for long-term savings but not for short-term emergency funds or cash.

Money Market Accounts

Money market accounts provide a secure and safe way to store savings with decent yields. They are insured by the FDIC for up to $250,000 per depositor, per insured bank. Unlike traditional savings accounts, money market accounts offer access via debit card or paper check. While they offer greater flexibility than traditional savings accounts and CDs, they typically pay less than CDs and require higher minimum balances.

Cash Management Accounts

Cash management accounts (CMA) are usually offered by non-bank financial institutions like brokerages and robo-advisor platforms. CMAs are not commonly available at banks and credit unions but can expand FDIC coverage beyond the $250,000 limit. These accounts typically pay lower interest rates than high-yield savings accounts.

Health Savings Accounts

A health savings account (HSA) is a tax-advantaged savings account designed to pay medical expenses. To open an HSA, you must be enrolled in a high-deductible health plan (HDHP) and contribute to it. Contribution limits vary, with individuals and families having a maximum contribution limit. Savers aged 55 and above can contribute an additional amount beyond the contribution limit. HSAs are not subject to federal income tax and unspent funds roll over for future healthcare expenses. However, they may not be suitable for everyone.

Types of Debt

Debt is the third component of financial literacy and involves money borrowed and repaid to a lender or creditor, with a contract specifying repayment dates and interest rates. Debt can be used to achieve goals like home purchases, college education, or car financing. However, it can also be a significant burden if taken on for the wrong reasons or without proper understanding. Different types of debt are best suited for specific purposes and goals. Understanding the various types of debt and using each type appropriately is crucial for becoming an informed borrower with strong financial literacy.

Secured vs. Unsecured Debt

Secured debt is a loan backed by valuable property, such as a house or car, which can be seized by the lender if payments are not made. Examples of secured debt include home mortgages and auto loans, which are tied to the value of the property purchased. If the borrower stops making payments, the lender can repossess the property, known as foreclosure, which is the process of repossessing the loan.

Unsecured debts, such as credit cards and medical bills, are loans without collateral, often found in personal loans, although some require collateral.

Revolving vs. Installment Debt

Revolving debt, like credit cards or home equity lines of credit, allows users to borrow and repay money up to a set credit limit, charging purchases and repaying the balance with interest. These debts typically have a minimum monthly payment and variable interest rates, with interest accruing on only the balance carried.

An installment loan is received in a lump sum and repaid in equal installments with a fixed interest rate, commonly used for personal, student, mortgage, and auto loans.

Good Debt vs Bad Debt

Good debt can be defined as debts which enables personal goals, provide security, stability, long-term financial gain, and the ability to build wealth.

For example, business loans, which require large initial investments, can be classified as good debt if they allow for the creation of a business that supports both the individual and their employees.

Bad debt can be categorized into credit card debt, high-interest loans, and loans for discretionary spending. Credit cards often have high interest rates, leading to carrying balances instead of paying them off monthly. High-interest loans, such as online installment loans, payday loans, and auto title loans, usually are associated with high fees or interest rates. Taking out loans for discretionary expenses like vacations or designer clothing can also be considered bad debt. It’s best to avoid certain types of loans to avoid a debt cycle where you constantly take out new loans to cover all your bills.

Credit Score

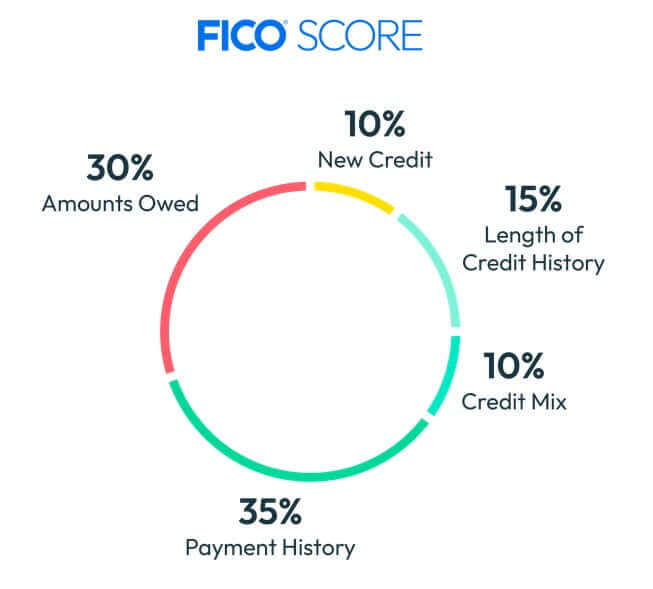

Credit scores are the fourth component of financial literacy and are crucial for lenders and credit card issuers to predict risk and ensuring the borrower’s repayment ability. The Fair Isaac Corporation (FICO) Score, used by a majority of top lenders in the US, analyzes credit reports to predict the likelihood of paying a bill 90 days late or worse within 24 months. The FICO scoring models rank credit reports on a scale of 300 to 850, with a higher score indicating a lower risk of falling behind on obligations, and a lower score indicating a higher risk of late payments.

Credit scores are based on information in your credit report, and factors like bank account balance, income, and net worth do not affect them. Factors which do impact your FICO score fall into five categories: Payment History (35%), Amounts Owed (30%), Length of Credit History (15%), New Credit (10%), and lastly Credit Mix (10%).

Payment History (35% of Score)

Your credit score is heavily influenced by your bill-paying history. While an on-time payment history is a good starting point, it doesn’t guarantee a perfect 850 FICO Score. A scoring model may inquire about late payments on the credit report, including their duration, the date, and the number of late payments. A 30-day late payment may not significantly impact your credit score if the rest of your report is in good shape. However, multiple late payments or severe late payments (60 days or worse) may cause a harder hit on your scores.

Amounts Owed (30% of Score)

Amounts Owed, sometimes referred to as credit utilization, accounts for 30% of your FICO Score. A scoring model may consider the total amount of debt on the credit report, how it breaks down among different types of accounts, and the total number of accounts with balances. Paying down credit card balances is beneficial for both your credit score and bank account, but large installment loans like mortgages, auto loans, and student loans may not have a significant impact on your credit score.

Length of Credit History (15% of Score)

Length of Credit History, is the third most influential category. FICO does not consider an individual’s age when calculating credit scores, however, the age of each debt accounts owed by an individual is considered. FICO scoring models ask questions about the ages of the newest and oldest accounts, the average age of all accounts combined, the length of time each account has been open, and the last active account. Time plays a crucial role in this credit report category, with older accounts and an older average age of accounts potentially helping to earn more points for overall credit score.

If someone adds you as an authorized user to an existing credit card or other debt account, the account may appear on your credit reports, potentially lengthening your average age of credit and potentially boosting your credit score.

New Credit (10% of Score)

Ten percent of your FICO Score is based on the New Credit category of your credit report, which includes recent inquiries. Hard inquiries, which appear on your credit report for 24 months, can affect your credit score for up to 12 months. Soft inquiries, which occur when you check your own credit or when a lender targets you for a pre-approved offer, do not impact your credit score. A scoring model may also consider the number of new accounts on your report and the open date of those accounts. It is advisable to only apply for and open new credit when needed, but leveraging your good credit rating to take advantage of attractive offers is also important.

Credit Mix (10% of Score)

The final category of a credit report is the Credit Mix. Managing multiple accounts can positively impact your credit score. A scoring model may consider the types of accounts on your report, such as credit cards, installment loans, retail accounts, mortgage loans, and finance company accounts. Having different types of credit accounts on a report will generally benefit the overall score.

Budgeting Strategies

A budget is the fifth component of financial literacy and is crucial for saving money, paying off debt, and fostering financial stability. However, creating an effective budget can be challenging without a clear plan or strategy.

50/30/20 Strategy

The 50/30/20 spending plan is a popular method consisting of three categories: Needs (50%), Discretionary Spending (30%), and Financial Goals (20%).

Needs include basic, non-negotiable expenses like housing, bills, groceries, and transportation. Discretionary Spending (30%) includes lifestyle spending like shopping, dining, and entertainment purchases. Financial goals (20%) involve money invested in savings accounts, debt repayment, or investments. This plan helps individuals manage their income effectively and achieve financial goals.

Zero-Based Strategy

A zero-based budget aims to give every dollar earned a purpose, ensuring monthly expenses equal income. This strategy involves preemptively identifying all expenses, categorization of those expenses, and how each dollar will be spent in a designated time frame.

However, this doesn’t mean spending every dime. It involves meticulous planning and tracking of spending categories, as well as a plan for leftover money and investments. Overspending in one category requires stopping spending until the next month or taking from another category. This approach encourages meticulousness in money management, ensuring that all income is spent efficiently.

Pay-Yourself-First Strategy

Pay-Yourself-First, sometimes referred to as “reverse budgeting” is a financial strategy which prioritizes meeting savings and debt goals by setting aside money for these goals first. This method allows you to use the remaining money for other purposes, while also accounting for recurring expenses like rent or mortgage payments and utilities.

Check out additional Investment Insights.