2 Divergent Economic Forecasts

Table of Contents

Divergent Paths Regarding Economic Forecasts

Federal Reserve Board Member, Michelle Bowman, expressed she disagreed with the Federal Open Market Committee’s (FOMC) economic forecast and decision to lower the federal funds rate target range by half a percentage. Instead, she recommended a 0.25% reduction compared to the 0.50% cut approved earlier this month. Furthermore, after the FOMC participant communications blackout period ended, the Board of Governors released Bowman’s statement explaining her departure from the majority of voting members. Bowman agreed, given the progress made in lowering inflation and cooling within the labor market since mid-2023, adjustments to the federal funds rate level was appropriate. However, she preferred a smaller initial cut in the policy rate, considering the U.S. economy remains strong and inflation remains a concern.

Economic Forecast from Board Member Michelle Bowman

Bowman warned the Committee’s policy action related to lowering inflation could be seen as a premature declaration of victory on the price-stability mandate. She emphasized the need to achieve low and stable inflation at the 2% goal to foster a strong labor market and an economy that works for everyone in the long term. Additionally, Bowman suggested moving at a measured pace (referring to the 0.25% reduction) toward a more neutral policy stance and closely monitoring labor market conditions to achieve further progress in bringing inflation down to the 2% target.

Labor Market – Michelle Bowman

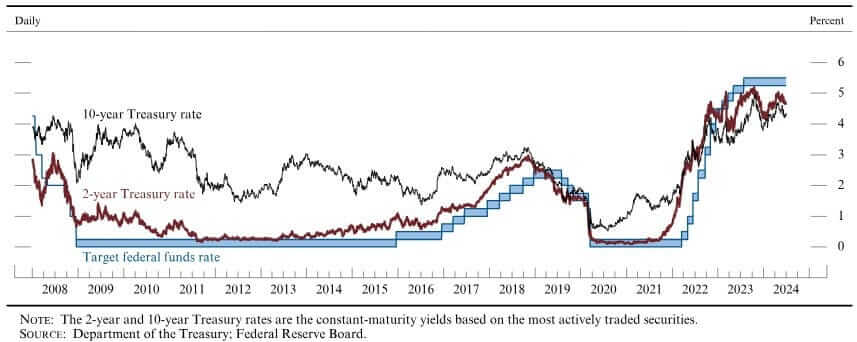

The labor market indicates payroll employment has slowed to slightly above 100,000 per month over the three months ending in August, while the unemployment rate edged down to 4.2% in August from 4.3% in July. Despite higher unemployment compared to a year ago, it remains at a historically low level. The labor market has loosened from tight conditions, with the ratio of job vacancies to unemployed workers declining to below the pre-pandemic level. This indicates a better balance between available workers and jobs. However, there are still more available jobs in relation to available workers, a situation only having occurred twice since World War II, indicating ongoing labor market strength.

Wage growth has slowed, just under 4%. The rise in unemployment this year is largely due to weaker hiring, longer job search times, and low layoffs. Factors contributing to increased unemployment include a mismatch between new workers’ skills and available jobs, suggesting a stronger supply of workers. Temporary factors, such as a sharp increase in unemployment among working-age teenagers in August, may also contribute to the situation. Overall, wage growth remains above the inflation goal due to trend productivity growth.

Inflation – Michelle Bowman

Inflation has been slowing down in recent months, with monthly readings lower compared to the first three months of the year. Core personal consumption expenditures (PCE) inflation has moved down since April, but remains above the 2 percent goal. High core inflation is largely due to pressures from housing prices, possibly due to low inventories of affordable housing. Progress in lowering inflation since April is welcome, however, core inflation remains above the Committee’s 2 percent goal. Moreover, prices remain higher compared to before the pandemic, affecting consumer sentiment, particularly for lower- and moderate-income households, who often devote a larger share of their income to food, energy, and housing.

Personal consumption has remained resilient, but consumers are pulling back on discretionary items and expenses, as evidenced by a decline in restaurant spending since late last year. Low- and moderate-income consumers no longer have extra savings to support discretionary spending, and loan delinquency rates have normalized from low levels during the pandemic.

Monetary Policy – Michelle Bowman

The U.S. economy is strong and core inflation remains above the 2 percent target. To adjust policy stance, a more measured approach is needed. Reducing the federal funds rate target range by 0.50% could signal fragility or greater downside risks to the economy. In the current economic environment, with no signs of material weakening or fragility, a 0.25% point move would have better reinforced economic conditions and recognized progress towards goals. A more measured approach would avoid unintentionally signaling concerns about underlying economic conditions.

Additionally, Bowman expressed concerns pertaining to the potential impact of reducing the policy rate on market participants, who may have expected the FOMC to lower the target range at future meetings until the policy rate reaches neutrality. This could lead to an unwarranted decline in interest rates and overly easing financial conditions, which could conflict with the Committee’s goal of returning inflation to its 2 percent target. Moreover, Bowman continued to express her belief there is a significant amount of pent-up demand and cash on the sidelines ready to be deployed as interest rates decrease. Immediate policy rate reduction could potentially unleash this demand, while a more measured approach would avoid over-stimulation and inflationary pressures.

Economic Forecast from Chair Jerome Powell

Federal Reserve Chair, Jerome Powell, provided an update on his perspective pertaining to the overall economic forecast. Powell explained the economy has made significant progress in the past two years towards achieving maximum employment and stable prices. Labor market conditions have cooled, and inflation has eased, with confidence in a sustainable path to 2 percent. The Federal Open Market Committee reduced policy restraint by lowering the target range of the federal funds rate by 1/2 percentage point, indicating with appropriate policy stance adjustments, strength in the labor market can be maintained in a moderate economic growth environment and sustainably lower inflation.

Labor Market – Jerome Powell

The labor market is robust, with a low unemployment rate, low layoffs, and a high labor force participation rate for individuals aged 25 to 54. The prime-age women’s participation rate has also reached new all-time highs. Real wages are increasing at a steady pace, and the ratio of job openings to unemployed workers has moved down but remains just above 1, indicating there are still more open positions than people seeking work.

The labor market has cooled over the past year, with workers viewing jobs as less available compared to 2019. This has led to a 4.2% unemployment rate, still low by historical standards. Further cooling is not necessary for 2% inflation.

Inflation – Jerome Powell

Over the past year, headline and core inflation have been 2.2% and 2.7%, respectively. Disinflation has been broad-based, with recent data showing progress towards a sustained return to 2.5%. Core goods prices have fallen 0.5%, close to pre-pandemic pace, as supply bottlenecks ease. Core services inflation is also close to pre-pandemic pace, with housing services inflation declining.

Monetary Policy – Jerome Powell

Over the past year, the United States has seen solid progress with the goal of restoring price stability without causing a rise in unemployment. Progress has continued in achieving this goal, however, inflation has remained above the target for the past three years. To address this, the United States has kept monetary policy restrictive, restoring the balance between supply and demand in the economy. This patient approach has paid off, with inflation now closer to the 2 percent objective and the risks to achieving employment and inflation goals now in balance.

The policy rate reached a two-decade high since the July 2023 meeting, with core inflation above 4% and unemployment at 3.5%. In the 14 months since, inflation has decreased and unemployment has increased, indicating the need for a policy stance adjustment. The decision to reduce the policy rate by 50 basis points is based on growing confidence where maintaining labor market strength in a moderate economic growth with sustained inflation of 2% is possible, with an appropriate policy stance.

Concluding Remarks from Board Member Bowman

Despite her dissent at the recent FOMC meeting and the communicated economic forecast, Bowman expressed appreciation toward her colleagues who chose to start the reduction in the federal funds rate with a larger initial cut in the policy rate target range. She also reiterated her commitment to continue working with her colleagues to ensure monetary policy is positioned to achieve maximum employment and return inflation to the desired target.

Additionally, Bowman communicated she will continue to monitor incoming data and information to assess the appropriate path of monetary policy, remaining cautious in adjusting the stance of policy. Monetary policy is not on a preset course, and decisions at each FOMC meeting are based on the incoming data and the implications for the economic forecast. The public should understand how deviations from the Fed’s goals inform policy decisions. By the next meeting in November, updated reports on inflation, employment, and economic activity will be received, along with a better understanding of how developments in longer-term interest rates and broader financial conditions might influence the economic forecast.

Lastly, Bowman concluded with reiterating her plans to visit with various business owners and others within her network to discuss economic conditions and assess the appropriateness of their monetary policy stance. She and the other members of the board remain concerned about inflation and emphasize the importance of price-stability and the risks of a labor market weakening. Restoring price stability is crucial for achieving maximum employment in the long run. If data indicates a labor market weakening, Bowman reinforced her support for adjusting monetary policy and taking action as appropriate.

Check out more Financial News Insights.